Homebuyers

Are VA Loans Assumable?

March 28, 2024

VA loans are a cornerstone for service members and veterans in homeownership, offering unparalleled benefits like competitive interest rates and no down payment requirements.

Among these benefits is the ability to assume a loan—passing it from one holder to another- representing a significant advantage.

This article will demystify the process of VA loan assumption, addressing its benefits, challenges, and the steps involved. Additionally, you'll learn about the impact on the existing and the new borrower, offering a concise roadmap through the nuanced landscape of VA loan assumption.

What Does it Mean for a VA Loan to be Assumable?

An assumable mortgage unlocks the possibility for a new borrower to step into the existing loan, inheriting the loan's terms and interest rate. This capability is a hallmark of VA loans, backed by the U.S. Department of Veterans Affairs.

For an assumable loan to transition smoothly from one bearer to the next, the main hurdle is the credit history of the aspiring homeowner. As part of the loan process, the new borrower's credit status will be vetted, ensuring that the prospective buyer is not only eligible but also prepared to uphold the financial legacy of the loan.

Thus, the integrity of one's credit history becomes essential, guiding the transition and illuminating the potential benefits and flexibility afforded to both the existing borrower and the prospective buyer.

Factors to Consider When Assuming a VA Loan

The key to understanding VA loan assumption is knowing the process and ensuring the new borrower has financial readiness, underscored by two pivotal factors: proof of income and a solid credit history.

Proof of income: The VA mandates a reliable income stream to manage monthly mortgage payments. A reliable income stream means documentation like pay stubs, tax returns, or bank statements, which paint a picture of financial stability.

Credit score: Ideally, you should have a score of 620 or above to meet VA's requirements. A lower score might not block your path but could steer you toward higher interest rates. Also, review your credit report because accuracy is critical—any discrepancies could hinder your approval process.

Pros and Cons of VA Loan Assumption

Embracing VA loan assumption presents both opportunities and caveats.

The Pros

The allure includes lower interest rates anchored in the loan's original terms rather than fluctuating market rates. This route also skirts closing costs, sparing you from extra charges like appraisal and origination fees. You might also find a repayment term extending up to 30 years, offering a broader timeline than many Conventional loans.

The Cons

However, this path could have its shadows. Assuming a loan could mean inheriting any outstanding debts left by the previous borrower, especially if they had defaulted. The VA predetermined the loan's conditions—its interest rate, amount, and term—limiting flexibility. Additionally, VA loan eligibility is specific, catering only to veterans, active-duty members, or their surviving spouses.

Potential VA Loan Assumption Challenges

When you take on a VA loan from someone else, two main challenges are dealing with home equity and understanding how it affects your VA loan benefits.

Home Equity

Firstly, if you're hoping to cash out some of the equity in your home through the loan, there's a catch. The VA sets a limit on how much money you can get based on the home's value and what you still owe on the loan. You also need to have enough equity in your home to begin with, which means you can't borrow more than the home is worth.

Your VA Benefits

Secondly, using a VA loan this way uses up your VA loan benefits, which is usually a one-time thing. If you take over someone else's VA loan, you're essentially using your VA benefit for that loan. Using your benefits in this way could be a drawback if you plan to buy another home with a VA loan in the future because you might have already used your entitlement.

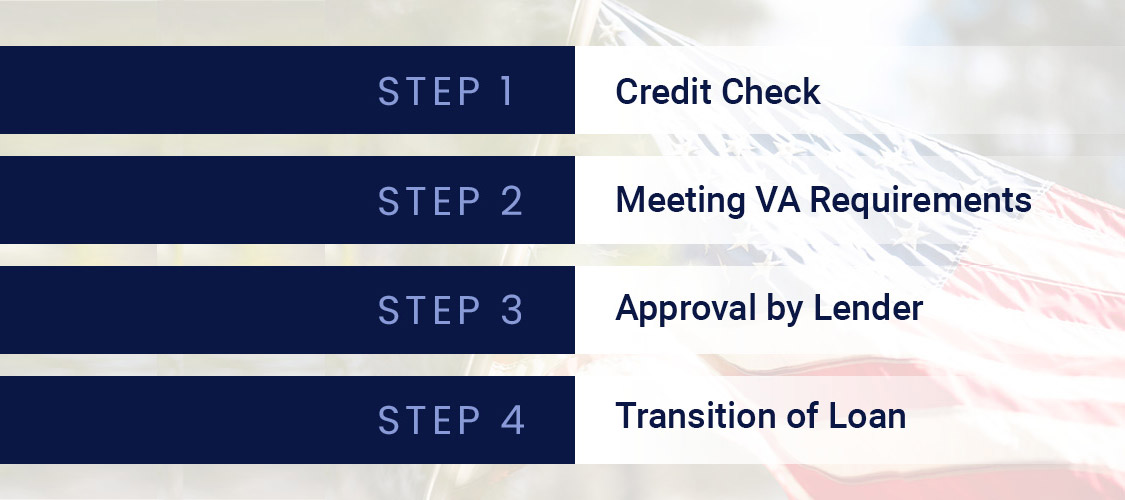

The Assumption Process for VA Loans

Taking over a VA loan involves a few straightforward steps, from getting the proper documents together to understanding what current and new loan holders need to do.

Step 1: If you're stepping into a VA loan, you'll need to get a Certificate of Eligibility (COE) from the VA. This certificate proves you meet all the VA's rules, like service time, credit score, and income levels.

Step 2: Apply for the loan with a lender. You'll need to hand in some paperwork, such as your COE, proof of your income, your credit score, and a valuation of the property you're taking the loan over for.

Step 3: The person giving up the loan will also need to provide some documents, including their original loan details and a statement showing how much they still owe.

Step 4: You'll sign the final papers, and then the original loan holder will be free from their mortgage, and you will become the property's new owner.

Impact on the Existing Borrower

When someone else takes over a VA loan, it brings a mix of outcomes for the original loan holder. The most noticeable change is that the original borrower no longer has the loan. That means no more mortgage payments or any other responsibilities linked to the loan. However, credit scores might also change. The loan assumption goes on the credit report, which could influence the ability to get loans or credit in the future. The lender can help, though. Often, the lender will help release you from the loan for a fee.

Your VA Loan Options

The VA loan assumption process is a strategic opportunity with distinct advantages and considerations for new and existing borrowers. While new borrowers can enjoy potential savings and a smoother path to homeownership, existing borrowers are relieved from their mortgages. Still, they must consider the impact on their credit and any associated fees. All involved must carefully weigh these factors to guarantee a successful and beneficial loan transition. Contact NAF to discuss your VA loan options today!

Author

Smart Moves Start Here.

Smart Moves Start Here.